HERE IS WHY

✓ Good growth potential for Indian pharmaceutical industry

✓ New products in the pipeline

✓ Impressive financial performance

Natco Pharma: Robustly Well-positioned

NSE: NATCOPHARM | BSE: 524816

Price: 840

The pharmaceutical industry in India is really important in the world.

According to a recent EY FICCI report, as there has been a growing consensus over providing new innovative therapies to patients, the Indian pharmaceutical market is expected to reach USD 65 billion by the end of 2024 and estimated to touch USD 130 billion in value by the end of 2030.

Considering the growth of the Indian pharmaceutical industry and to participate in it, our choice scrip recommendation for this issue is Natco Pharma. Incorporated in 1981, Natco Pharma is a vertically integrated pharmaceutical company engaged in developing, manufacturing and marketing complex products of pharmaceutical formulations and APIs.

Operating from eight manufacturing facilities and the Natco Research Centre in Hyderabad, the company’s formulations units in Kothur (Telangana) and Visakhapatnam (Andhra Pradesh), along with API facilities in Chennai and Mekaguda (Telangana), hold approvals from regulatory bodies, including the USFDA. Diversifying its portfolio, Natco Pharma has established an agrochemicals facility in Nellore (Andhra Pradesh). For the quarter ended September 30, 2023, the company’s formulation business contributed 84.35 per cent to the total revenue followed by API (domestic and exports, 7.33 per cent), crop health sciences (5.26 per cent) while other operating and non-operating incomes contributed the rest.

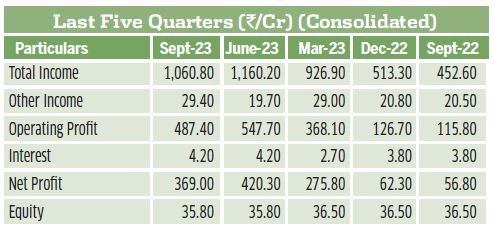

In Q2FY24, on a consolidated basis, the net revenue rose by 138.69 per cent YoY to ₹1,031.40 crore compared to ₹432.10 crore from the previous year’s same quarter. On a sequential basis, revenue decreased by 9.57 per cent from ₹1,140.50 crore. For Q2FY24, the PBIDT excluding other income increased by 380.59 per cent and was ₹458 crore from ₹95.30 crore in the previous year’s same quarter. The profit after tax (PAT) showed growth of 549.65 per cent and stands at ₹369 crore from ₹56.80 crore in the previous year’s same quarter. On a sequential basis, the net profit decreased by 12.21 per cent from ₹420.30 crore.

The company has a pipeline of new products, including Semaglutide and Olaparib, which are under review. The company’s research and development investments are expected to continue to support the development of a strong pipeline of new products. The company aims to sustain and improve its margins in the coming years through product launches and market expansion. It is actively looking for inorganic growth opportunities and has a strong cash position. The company commands a robust presence in the complex generics space and has strong research and development capabilities.

It also enjoys a dominant market position in domestic oncology along with anticipated improvements in the crop health sciences segment, which collectively contribute to a promising growth outlook, particularly in non-US geographies. The company is currently trading at a PE of 13.8 times as against the industry PE of 35.9 times and lower than its three-year median PE of 31.2 times. Considering the company’s business and potential, we recommend closely watch this stock for potential upside in next one year.