W&C company stocks have shown impressive performance on the stock market. RR Kabel’s shares have surged by over 50% from its initial price of ₹1,035 per share.

The wires & cables (W&C) industry is prospering due to the government’s focus on infrastructure and rural electrification, as well as growth in commercial and residential sectors, 5G rollout, and digitization. Furthermore, the industry benefits from increasing consumer demand for product upgrades and replacements.

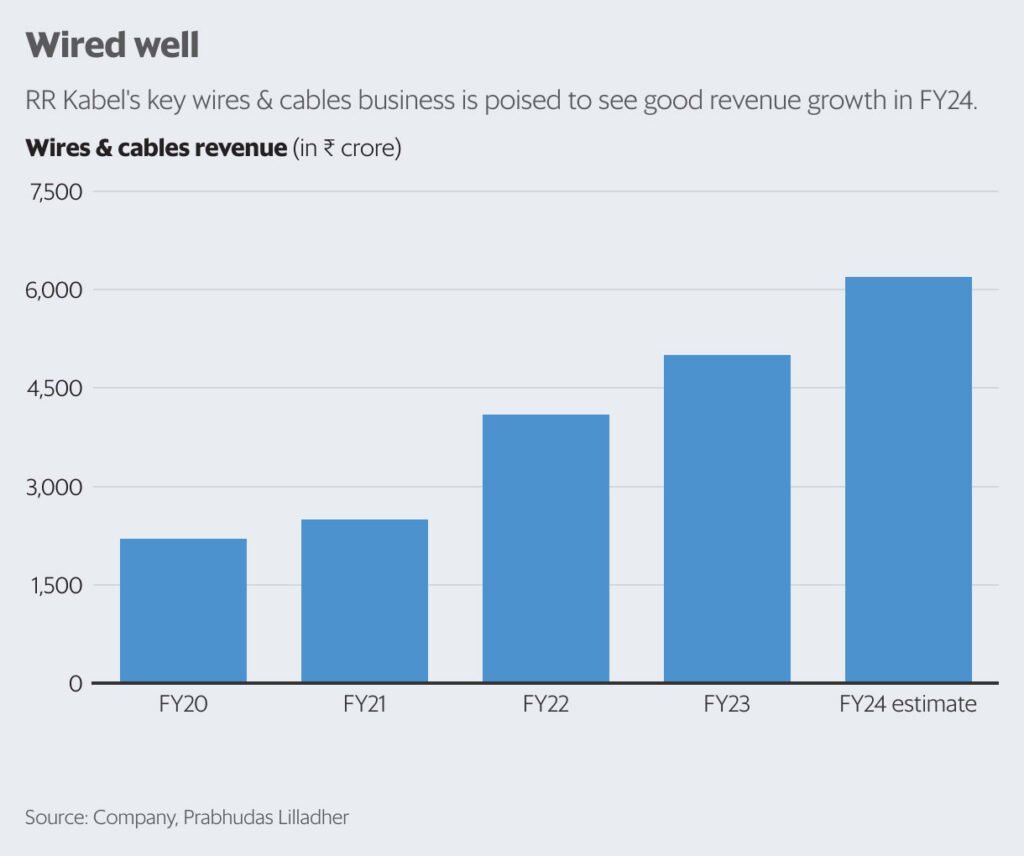

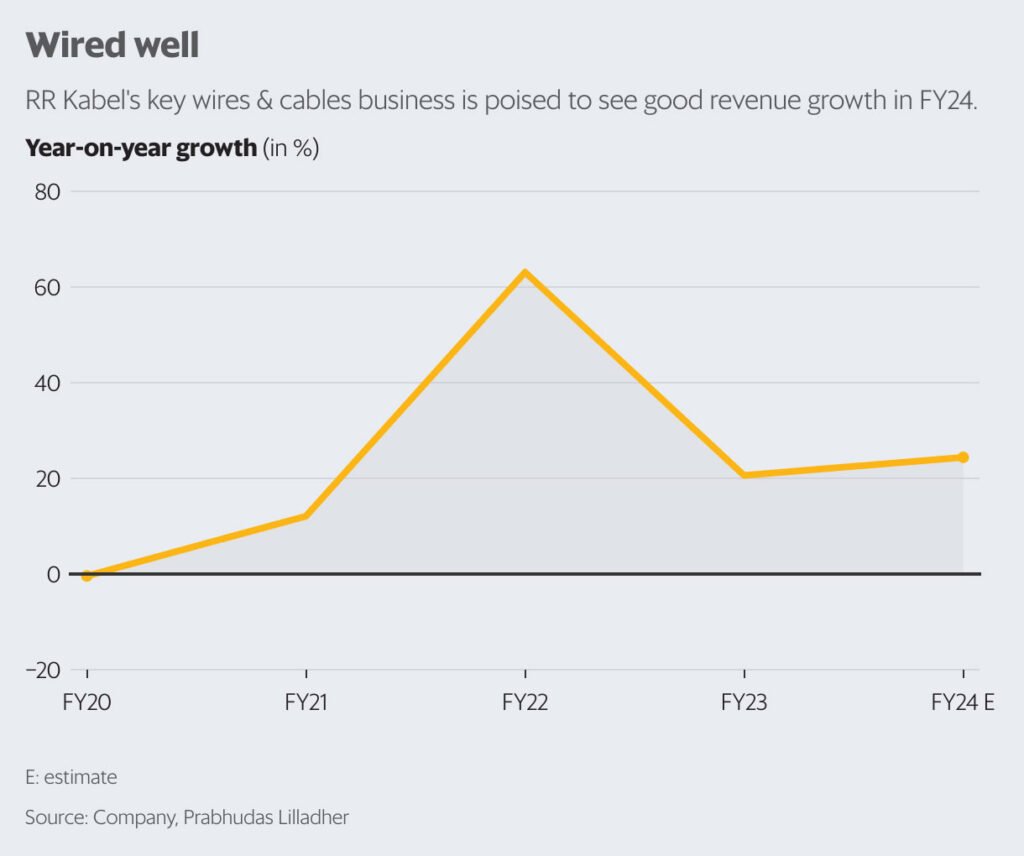

Against this backdrop, W&C companies’ stocks have performed well on the stock market. RR Kabel Ltd (RR), a key player in the sector that debuted on 20 September, has seen its stock rise by over 50% from its issue price of ₹1,035 per share. The company’s strong profitability in the September quarter (Q2FY24) contributed to this growth. The Ebitda margin increased by 44 basis points sequentially to 7.5% in Q2, driven by improved volume performance in the W&C business, which accounted for 90% of gross segment revenue, with the remainder coming from the fast-moving electrical goods (FMEG) segment.

In the W&C sector, RR has sustained a healthy volume growth projection of 15-20%, and anticipates a 10% margin in the short term, owing to a strong demand outlook in various sectors and efforts to enhance margins,” as highlighted by Praveen Sahay, an analyst at Prabhudas Lilladher.

During the FY23-FY26 period, there is an expectation of annual compounded growth in revenue, Ebitda, and net profit at 21.7%, 41%, and 46% respectively.

Additionally, RR has established a significant presence in exports, contributing approximately 28% to the overall revenue in H1. The company is witnessing robust demand in export markets and anticipates substantial growth in the short term.

As of FY23, RR held a 9% share in the export market. According to Sahay, RR exports a substantial quantity of cables, which yield high margins. Therefore, the decision by RR to double its power cable capacity is well-founded.

The current trading of RR’s shares at 40 times the estimated earnings for FY25 seems relatively high. Going forward, investors should closely monitor demand trends in end-user industries such as real estate. Moreover, heightened competition and price volatility of key raw materials like copper and aluminium could potentially impact RR’s profitability.

Furthermore, the FMEG (Fast Moving Electrical Goods) business recorded a 20% year-on-year revenue growth in H1, attributed to the contribution from Luminous Power’s home electrical business, which was acquired in May 2022. However, the segment is incurring losses due to elevated fixed costs and lower capacity utilization.

The overall decline in consumption has exerted pressure on the FMEG segment.

Should there be an improvement in the performance of the FMEG segment, investors are likely to view this favorably and it may attract positive attention.