The investment sentiment showed improvement in the December quarter, albeit weaker compared to the same period last year. Analysts anticipate a mixed outlook amid the approaching Lok Sabha elections, yet the overall trend reflects optimism.

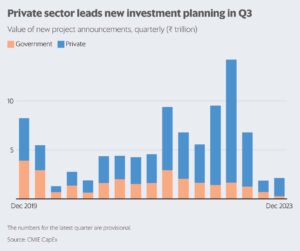

Green shoots are becoming visible for the Indian economy as it steps into 2024, with the recently concluded quarter showing long-awaited signs of revival in the investment cycle. According to data from the project-tracking database of the Centre for Monitoring Indian Economy (CMIE), a total of ₹2.1 trillion worth of new projects were announced in the December-ended quarter, marking a nearly 15% increase from the previous three-month period.

Although the capital expenditure proposals were still considerably lower than the figures from a year ago, which saw projects worth ₹9.5 trillion being announced, the recent data indicates a significant turnaround following two quarters of steep decline. It’s worth noting that the data is provisional and subject to potential updates in the future.

In a positive shift, private companies have taken the lead this time around. Among the most prominent private sector announcements are JSW Neo Energy’s pumped storage power project in Almora valued at ₹15,000 crore and Welspun New Energy’s Green Ammonia manufacturing unit project in Odisha worth ₹13,860 crore.

“New investment proposals are being supported by the expectation of policy continuity at the Centre post the Lok Sabha polls later this year,” explained Anitha Rangan, an economist at Equirus. “This assumption forms the basis for positive projections, especially following the recent state election results, which have further solidified this view, thereby bolstering the investment cycle.”

In contrast, the public sector’s inclination towards initiating new capital expenditure planning has continued to decline. According to Suvodeep Rakshit, senior economist at Kotak Institutional Equities, the potential for a sustained government capex thrust is now diminishing as the Centre’s focus shifts back to fiscal consolidation.

Manufacturing Investment Trends: An Overview

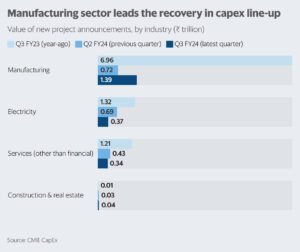

The investment climate showed signs of improvement, with a notable focus on manufacturing. Manufacturing accounted for nearly 65% of the value of new project announcements, marking a substantial 94% increase sequentially. However, other segments experienced a decline of 34.4% in combined proposals. It’s worth noting that the value of capex proposals in manufacturing also decreased by 80% compared to the previous year.

A significant portion of the manufacturing investment plans during the December-ended quarter was dedicated to projects in the inorganic chemicals sector, particularly in the areas of green ammonia and green hydrogen. Notable announcements came from the Welspun group, Tata Steel, and Sembcorp Green Hydrogen. Additionally, there is an anticipation of specific capex related to the electric vehicle ecosystem, solar, and wind energy due to technological shifts surrounding the green energy theme, as highlighted by Rangan.

In contrast, the construction and real estate space witnessed a substantial 59% quarter-on-quarter increase and showed a remarkable over fivefold growth on a year-on-year basis. Meanwhile, sectors such as electricity and services (excluding financial services) experienced declines of over 20% sequentially, with projects worth approximately ₹37,000 crore and ₹34,000 crore announced in these respective sectors during the period. Although there is an overall growth trend, Rakshit cautioned that domestic private consumption remains subdued. Furthermore, a potential gradual slowdown in global demand may impact the private investment cycle. These factors highlight the need for continued monitoring and adaptation to navigate potential challenges in the investment landscape.

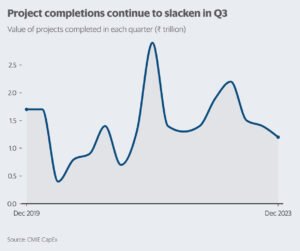

Challenges with project completions

Despite an increase in new proposals, the completion of existing projects has encountered difficulties. In the December quarter, approximately ₹1.2 trillion worth of projects were completed, reflecting a decrease from the average of ₹1.7 trillion completed quarterly in 2023. This marked a significant decline of nearly 15% following a 7% contraction in the previous quarter, representing the third consecutive decrease. Additionally, the value of completed projects was 34% lower than the previous year’s period.

Looking ahead, some analysts anticipate a mixed near-term investment outlook due to the upcoming 2024 election season, which could lead to potential halts or delays in new project approvals amidst the Lok Sabha elections. Nevertheless, structural enablers such as shifts in consumption patterns, technology, and global supply chains, along with the prospect of domestic policy continuity, are poised to support long-term growth.